How to Avoid the RMD Tax Trap

When you approach retirement, understanding Required Minimum Distributions (RMDs) becomes crucial. RMDs are the minimum amounts you must withdraw annually from your retirement accounts after reaching a certain age, traditionally set by government regulations to ensure that investments in tax-advantaged accounts don’t just accumulate but are eventually taxed.

This regulation affects various accounts, including 401(k)s, traditional IRAs, and other types, such as 403(b)s, which require withdrawals to ensure these savings contribute to your taxable income during retirement. Learning how to avoid the RMD tax trap can save you thousands in unnecessary taxes and penalties.

Grasping the nuances of RMDs is essential not just for compliance but also to sidestep hefty penalties and unnecessary taxation. If overlooked or mismanaged, the implications can include a tax penalty as severe as 25% of the amount that should have been withdrawn, in addition to the regular income tax on the distributions.

Familiarizing yourself with the specifics of RMDs and integrating this knowledge into your financial planning can safeguard you from unexpected fiscal burdens. By proactive management and understanding of RMDs, you can maintain greater control over your financial health in retirement, ensuring that you can enjoy your later years with economic security and peace of mind.

Understanding RMDs

Required Minimum Distributions (RMDs) are amounts that you must annually withdraw from your retirement accounts once you reach a certain age, ensuring that your savings, which have benefitted from tax-deferred growth, are eventually taxed. This rule primarily affects holders of traditional IRAs, 401(k) plans, and 403(b) plans, among other tax-deferred retirement accounts.

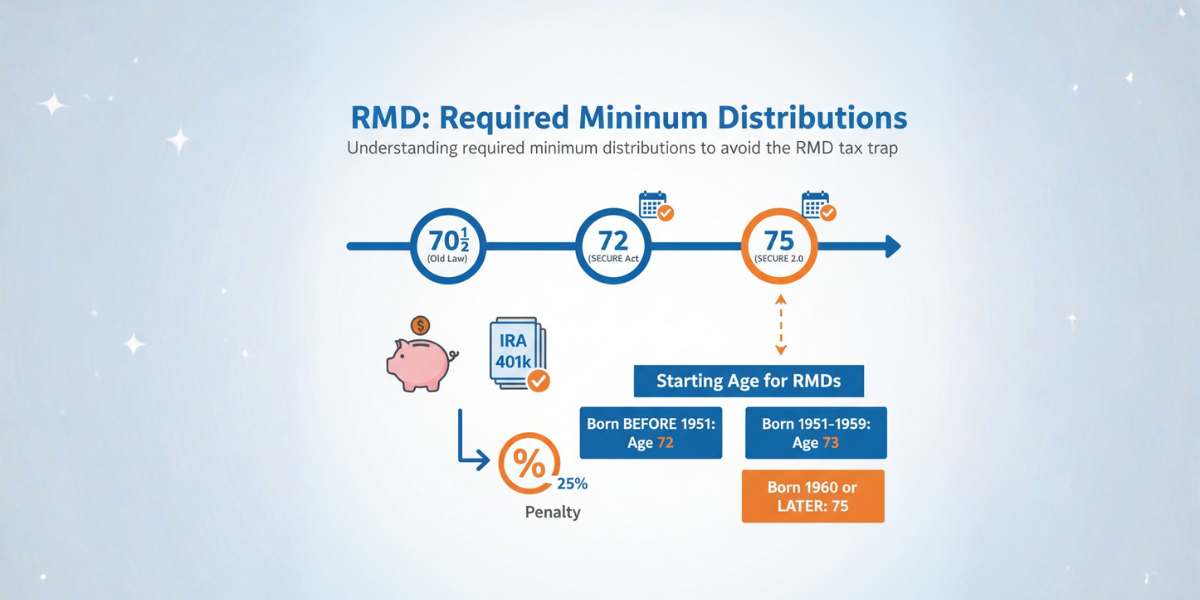

You must start taking these distributions at a specific age, which has recently been subject to legislative changes. Initially set at 70 ½, the SECURE 2.0 Act has increased this age to 73 for individuals born on or after January 1, 1951 and before January 1, 1960.

For those born after December 31,1959, RMD’s do not need to be taken until age 75. Understanding when to begin taking your RMDs is important, as failing to comply can result in significant penalties, typically amounting to 25% of the amount that should have been withdrawn.

This mandate ensures that these tax-advantaged savings don’t simply accumulate indefinitely without being taxed, promoting a steady flow of revenue from older taxpayers back into the economy. When you avoid the RMD tax trap through proper planning, you can potentially maintain more of your retirement savings for your future needs.

The Impact of RMDs on Your Taxes

When you start withdrawing your Required Minimum Distributions (RMDs), it’s important to understand how these withdrawals impact your taxes and how much you pay. RMDs are taxed as ordinary income, which means they’re added to your total income for the year and taxed at your applicable rate.

This additional income could potentially push you into a higher tax bracket, increasing not only the tax rate on your RMDs but also on your other sources of income. For example, if your RMDs move you from the 22% tax bracket to the 24% bracket, your tax liabilities could see a significant increase, affecting your overall financial strategy for the year.

You need to plan these distributions carefully and consider their timing, especially in years when you might have other substantial income sources. Strategic planning can help manage your tax bracket and reduce the total tax liability associated with your RMDs, ensuring more of your hard-earned money stays in your pocket or continues to grow for your future needs.

Key Dates and Deadlines

Navigating the timeline for Required Minimum Distributions (RMDs) is important to ensure compliance with IRS regulations and avoid substantial penalties. As you approach retirement, mark your calendar with these critical deadlines to avoid the RMD tax trap.

You must take your first RMD by April 1 of the year following the year you turn 73. This is a shift from the previous age of 70½, thanks to recent legislation.

For all subsequent years, including the year in which you took your first RMD by April 1, you are required to take your RMDs by December 31. Missing these deadlines can lead to significant financial consequences.

The IRS imposes a penalty of 25% on the amount you failed to withdraw (reduced from 50% under SECURE 2.0) as required. For example, if you were supposed to withdraw $10,000 and missed the deadline, you could be hit with a $2,500 penalty.

Keep these dates in mind and plan your withdrawals accordingly to avoid unnecessary fines and stress. Remember, it’s not just about meeting deadlines; it’s about strategically planning for your financial future in retirement.

Strategies to Minimize RMDs

When planning your retirement finances, you might find it beneficial to delay withdrawals from your retirement accounts if immediate funds are not required for your retirement expenses. This strategy not only allows your investments more time to grow but also potentially reduces the total amount you must withdraw once you reach the age for Required Minimum Distributions (RMDs).

You may want to consider converting your traditional IRAs to Roth IRAs. Unlike traditional IRAs, Roth IRAs do not require withdrawals until after the owner’s death, which can significantly reduce your immediate taxable income and future RMDs.

This conversion involves paying tax on the converted amount during the year of conversion, so it’s vital to analyze if future tax savings from reduced RMDs will offset this upfront cost. This strategic move can be especially advantageous if you expect to be in a lower tax bracket in the year of conversion compared to future years.

By utilizing these strategies to avoid the RMD tax trap, you can maintain a larger corpus in your retirement accounts for a longer period. This approach potentially reduces your lifetime tax liability and increases the financial legacy you might leave behind.

Using RMDs Wisely

When managing your Required Minimum Distributions (RMDs), consider using this income stream in a variety of beneficial financial moves. Redirecting RMDs into taxable accounts can be a strategic choice.

This action lets you continue the growth potential of your investments, diversifying your portfolio into assets that might not fit within traditional retirement accounts. You may also want to consider the benefits of using RMDs to fund life insurance.

This can particularly benefit your heirs by providing them with a tax-free inheritance, depending on the policy and other factors. Another smart way to utilize RMDs is through charitable donations, known as Qualified Charitable Distributions (QCDs).

Opting for a QCD allows you to donate all or a portion of your RMD to a qualified charity tax-free, which not only helps you meet your philanthropic goals but can also offer significant tax benefits. This method directly reduces the taxable income associated with your RMDs, potentially keeping you in a lower tax bracket and easing your overall tax burden.

By carefully planning what to do with your RMDs, you can ensure these funds continue to work for your financial wellness and legacy goals. This strategic approach helps you avoid the RMD tax trap while maximizing the value of your retirement distributions.

Legal and Financial Tools for Managing RMDs

When it comes to managing Required Minimum Distributions (RMDs) efficiently, incorporating legal and financial tools such as trusts and annuities can be instrumental. Trusts, specifically, offer a structured way to control how your retirement funds are distributed after your passing, potentially minimizing estate taxes and ensuring that your heirs receive their due without the additional burden of tax inefficiencies.

By designating a trust as the beneficiary of your retirement accounts, you can craft detailed rules about how and when the assets are passed to your heirs. This might include spreading out distributions over several years to reduce the tax impact.

Annuities offer a distinct type of financial management tool. By purchasing an annuity, you convert a lump sum of money into a stream of payments that can be extended throughout your retirement years.

This can strategically align with RMD requirements, ensuring that you adhere to legal withdrawal mandates while stabilizing your income. Annuities can be beneficial if you are concerned about outliving your assets, as they can provide a guaranteed income irrespective of market conditions.

A financial advisor plays a crucial role in navigating these options. They can help analyze whether these tools align with your overall retirement and estate planning goals and assist in the intricate process of setting these instruments up correctly.

Consulting a financial advisor can lead to a tailored approach that incorporates your unique financial situation, your tax obligations, and your future wishes for your estate. A combination of the right tools and expert advice is essential to optimize your financial strategy concerning RMDs.

Examples of Effective RMD Management

When you manage your Required Minimum Distributions (RMDs) efficiently, it can make a significant difference in your tax liabilities and financial health during retirement. Consider the case of Jane, a retiree who started strategizing her RMDs well before the required beginning date.

She divided her IRA investments between bonds and stocks, planning to withdraw from the bond portion during market downturns to prevent selling stocks in a low market. This strategy not only created steady income but also minimized the impact on her investment balance, optimizing her tax situation by keeping her in a lower tax bracket.

Another effective example is Bob, who used his RMDs for charitable contributions. By opting for a qualified charitable distribution (QCD), he directed his RMDs directly to a qualified charity, thus excluding that income from his taxable income.

This move not only fulfilled his desire to contribute to a cause but also kept his Medicare premiums lower, as your reported income influences these. Bob’s approach demonstrates one practical way to avoid the RMD tax trap while supporting charitable causes.

Sarah and Tom, a married couple, consulted with a financial advisor to evaluate the potential of a Roth IRA conversion. By gradually converting their traditional IRA to a Roth IRA, they managed to decrease the balance in their traditional IRA, subsequently reducing the size of their future RMDs.

This careful planning helps them to manage their tax brackets more efficiently, especially since Roth IRA distributions do not count as taxable income. These examples illustrate how personalized strategies for managing RMDs can yield tangible benefits.

Whether it’s using RMDs for charitable giving, strategic withdrawals, or converting to Roth IRAs, understanding and planning your distributions can significantly mitigate tax hits. This approach enhances your financial flexibility in retirement.

Planning for Unforeseen Circumstances

As you navigate the waters of Required Minimum Distributions (RMDs), it’s crucial to consider how unexpected life events might alter your meticulously laid plans. Whether you opt for early retirement, encounter health issues, or change marital status, each of these scenarios can significantly impact your RMD strategy.

In the face of early retirement, your timeline for beginning RMDs might shift, potentially affecting your financial landscape earlier than anticipated. Health complications could also alter your income needs, prompting a reassessment of how and when to draw upon your retirement savings.

Changes in marital status, such as divorce or the death of a spouse, can necessitate a reevaluation of your financial strategy to ensure it accurately reflects your new circumstances. To maintain flexibility in your financial planning, stay proactive by revisiting and adjusting your plans regularly.

This dynamic approach ensures that your RMDs align with your current needs and goals, despite the unpredictable nature of life. By incorporating a degree of flexibility into your RMD planning, you can more effectively respond to life’s uncertainties without compromising your financial security.

Maintaining Compliance and Records

Ensuring accuracy in record-keeping and maintaining diligent documentation of your Required Minimum Distributions (RMDs) are critical to staying compliant with IRS regulations and being prepared for any potential audits. Every withdrawal from your retirement accounts, particularly those required as RMDs, must be thoroughly documented.

Keeping impeccable records will not only help you track the annual withdrawals to satisfy the RMD requirements but also provide essential support if discrepancies arise during tax filings. Constant interactions with tax professionals can significantly benefit you.

These experts can give current guidance tailored to evolving tax laws and RMD requirements, ensuring you stay up-to-date. Leveraging their expertise can be especially helpful during tax season to verify that all distributions have been reported correctly and that you are utilizing all available opportunities to minimize tax liabilities.

Regular consultation also prepares you to respond effectively to any IRS inquiries, providing peace of mind that your retirement fund management aligns with legal requirements. Proactive management and expert advice are your best tools in ensuring full compliance and optimal handling of your RMDs.

Key Takeaways for Retirement Success

As you approach or navigate through the phase of retirement, understanding the dynamics of Required Minimum Distributions (RMDs) becomes crucial. This knowledge not only ensures compliance with federal regulations but also provides strategic benefits that can significantly impact your financial well-being in the years to come.

Preparation is key to managing your retirement accounts effectively. Starting with comprehending what RMDs are and the retirement accounts they affect is fundamental.

Accounts such as IRAs, 401(k)s, and 403(b)s are all subject to RMDs. By knowing the types of accounts and the legislation affecting them, you position yourself to manage your retirement savings better.

Strategic timing matters significantly when it comes to RMDs. The alteration in age requirements for RMDs necessitates a close watch on key dates and deadlines.

Missing these can lead to hefty penalties. Strategically planning the timing of your first and subsequent RMDs can lead to more favorable tax outcomes and more efficient financial planning.

Understanding tax implications is essential for retirement planning. Since RMDs are taxed as ordinary income, they could potentially nudge you into a higher tax bracket, increasing your overall tax liability.

Awareness and understanding of how these distributions affect your taxes allow you to take proactive measures to lower your tax obligations potentially. Smart management and wise use of your distributions can make a substantial difference.

You can employ several strategies to minimize the impact of RMDs. These include delaying withdrawals if your retirement finances permit, or converting traditional IRAs to Roth IRAs for future tax benefits.

The wise use of these distributions, whether reinvesting them, using them for charitable donations, or funding insurance, can extend the value and utility of your RMDs. Professional guidance through financial advisors and legal tools like trusts and annuities should not be underestimated.

Professional advice is invaluable, offering tailored strategies that encompass trusts, annuities, and other legal instruments to effectively manage and distribute retirement funds. Implementing comprehensive tax strategies allows you to adapt to life’s unpredictable nature.

Adjusting your financial and retirement plans due to life changes such as health issues or changes in marital status is sometimes necessary. Staying adaptable allows you to maintain financial stability despite these changes.

Documentation and compliance cannot be overlooked in retirement planning. Stringent record-keeping and regular consultations with tax professionals ensure that you stay compliant with all requirements concerning RMDs.

Proper documentation shields you against potential audits and penalties, securing your financial legacy. By embracing these practices and strategies, you are better equipped to manage your RMDs efficiently, minimizing unnecessary penalties and maximizing your financial well-being during an essential phase of your life.

Armed with this information, you can approach RMDs not just as a statutory obligation, but as an opportunity to refine and enhance your retirement strategy. Understanding how to avoid the RMD tax trap empowers you to take control of your retirement income and build lasting financial security.