If you want to build wealth and optimize your financial life, hiring a financial advisor can be a smart move. Unfortunately, not all financial advisors are equal – not by a long shot. And if you hire someone who isn’t qualified, you could wind up worse off than when you started.

1. Not Understanding How an Advisor Is Paid

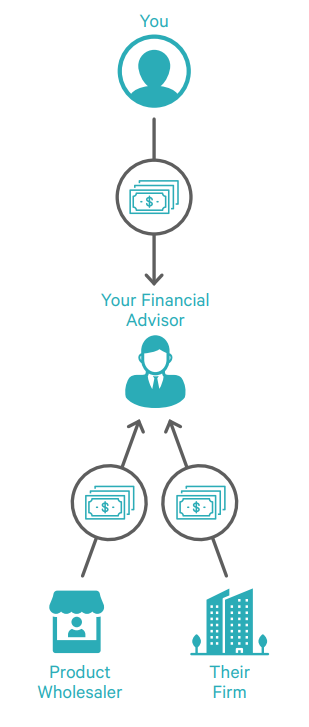

Financial planning and investment costs can be confusing, and it’s not uncommon for financial advisors to not readily disclose their fees. But you can’t have a trusting working relationship with someone without fully understanding how they are being compensated.

Are you paying the advisor directly? Do they earn commissions from their firm or another product wholesaler? It’s one thing to know how you are paying the advisor, it’s another thing entirely to understand how the advisor is paid from all sources. Are there incentives for the

advisor to act in ways that go against your best interest?

Not only can this mistake cause you to work with an advisor who has conflicts of interests, but it can also lead to wasted money in the form of unnecessary fees and expenses.

Do the due diligence to understand the nuances of an advisor’s pay structure. The common phrase “Follow the money” tells us that we can learn a lot about a person’s motivations based on how they are paid.

2. Not Checking Credentials & Background

Credentials and education play a critical role in your advisor’s competence, and many people mistakenly assume that everyone who calls themselves a financial advisor has a certain level of education and expertise.

Although there are over 200,000 financial advisors in the U.S., only 25% of financial advisors hold the CFP® designation. Anyone can provide financial planning (and becoming a financial advisor is actually not that hard, you just need to pass a securities exam and get hired by a large brokerage firm), but the CFP Board states that unless someone is a CERTIFIED FINANCIAL PLANNER™ professional, the quality and accuracy of the financial plan are not guaranteed.

There are hundreds of designations in the financial services field, some of which have more stringent requirements than others, and education, credentials, and licenses can change the nature and quality of the services provided as well as the legal rights you would have should anything go wrong.

The Gold Standard of Designations

The CFP® certification is considered the industry standard for financial planners for

several reasons:

- The CFP Board requirements are much higher than simply passing a securities exam, including a more comprehensive education, higher standards, experience, and ongoing ethical requirements.

- CFP® professionals are taught to take a holistic approach to wealth management.

- CFP® professionals assist with a wide array of financial aspects, including investments, retirement planning, insurance planning, tax planning, charitable giving strategies, and more.

- CFP® professionals are trained to help you plan around every aspect of your financial life (while a typical financial advisor likely has much less expertise).

CFP® Board Requirements are much higher than simply passing a securities exam. A college degree is also a requirement for CFP® professionals.

3. Hiring an Advisor With the Wrong Specialty

Some financial advisors focus on serving a specific demographic or level of investable assets, while others provide more general service. It’s important to understand this up front so you know you’re paying for advice and services that are tailored to your unique needs.

Advisor specialties are not just a nice cherry on top of the financial planning relationship. Instead, it should be one of your most essential considerations. In all likelihood, there’s an advisor out there who specializes in serving your particular needs—and it’s worth the extra due diligence to find them.

It’s also important to not blindly hire advisors with licenses or specialties you don’t understand. For example, you may think you are being more efficient by hiring an advisor who also has an insurance license, but in reality, you could be creating a constant conflict of interest for your advisor and yourself. How will you ever really know if they are recommending insurance because it’s in your best interest versus recommending it because they get a commission?

Having more licenses or designations doesn’t always mean better. Instead, be intentional about the designations, licenses, and specialties you are looking to work with.

4. Failing to Discuss Investment Philosophy

Many people seek out financial and investment advice because they don’t know much about the industry themselves. Because of that, they often don’t know the right questions to ask or topics to bring up to make sure the advisor they hire really makes sense for their situation.

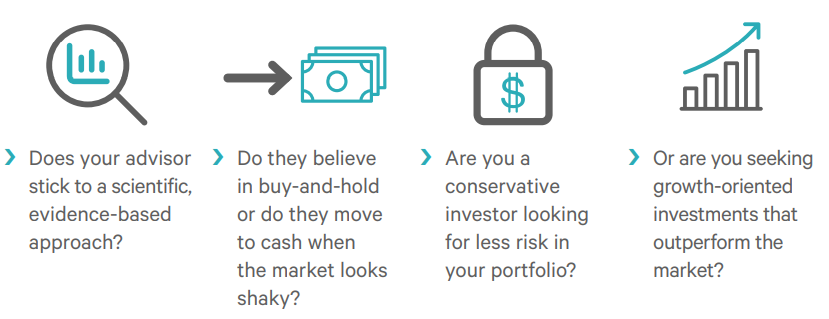

One of the most critical topics to cover in the due diligence process is the advisor’s investment philosophy.

It’s important to work with an advisor who shares a planning and investing philosophy similar to your own:

The answer to these questions will make a difference in the type of advisor you should work with. Take the time to understand how your advisor guides clients’ investing and financial decisions before you commit to their services. The last thing you want to do is sign up for a service that is fundamentally incompatible with your investment philosophy.

A good advisor will help you understand what you are looking for and whether or not they can meet your investment needs.

5. Believing an Advisor Who Is Trying to Beat the Market

If you’ve ever spent time looking for a financial advisor, you’ve probably heard at least some of them claim that their investment strategies can “beat the market.” It can be enticing to think about how much money you can make working with an advisor who

promises extraordinary returns with little downside risk. But if something sounds too good to be true, it usually is; and beating the market is no exception.

In fact, a new study reports that nearly 80% of active fund managers are underperforming their benchmarks. That means that while some actively managed funds had higher returns than their comparable index, the vast majority did not. Instead of working with an

advisor who is trying to beat the market, clients should focus their attention, time, and energy on finding an advisor who:

6. Confusing the Terms Fee-Based and Fee-Only, Broker-Dealer, and Financial Planner

Another common mistake people make is confusing several key terms that are important in understanding who you are working with and how they do business. These include:

- Fee-only: In this model, the advisor only charges a fee for service. It can be an hourly fee, a flat fee, or a percentage of assets under management. Because the fee-only model has no conflicts of interest, it is generally considered the fiduciary fee model.

- Fee-based: This compensation method combines fee-only and commissions. An advisor will charge a fee for services, but may also receive a commission if they sell you a product (insurance, annuity, investment). Because you never know if the advisor is recommending a product just to receive a commission, this fee model has constant conflicts of interest.

- Broker-dealer: A broker-dealer facilitates the buying and selling of investments like stocks and bonds. They will first act as a dealer to buy investment offerings from companies, then they act as a broker to sell those investments to the public. In addition to buying and selling investments, broker-dealers also offer financial advice, which is usually limited to investments. Broker-dealers are not held to the fiduciary standard. Instead, they must meet the less strict suitability standard, which states investment recommendations have to be suitable for clients but not necessarily in their best interest.

- Financial planner: Anyone can call themselves a financial planner who seeks to help clients achieve their long-term financial goals. But, as mentioned above, the CERTIFIED FINANCIAL PLANNER™ designation signals the industry’s gold standard for financial planners. CFP® professionals are held to the fiduciary standard, which is a strict ethical standard that means they must put their clients’ interests ahead of their own as they look at all aspects of their finances, including retirement, investments, taxes, risk management, and estate planning to build a comprehensive plan.

As you can see, the difference between these terms makes a huge difference in the type of service you will receive.

7. Choosing an Advisor Who Isn’t a Fiduciary 100% of the Time

This mistake goes hand-in-hand with #6. Without properly understanding what these terms mean, you may find yourself working with someone who isn’t actually a CERTIFIED FINANCIAL PLANNER™. You might be paying fees and commissions when you wanted to pay fee-only, and you may find your investment recommendations are only subject to the suitability standard when you wanted to work with a fiduciary.

An advisor who serves as a fiduciary accepts a responsibility to put his or her clients’ interests first and foremost in all decisions. A fiduciary is legally required to disclose conflicts of interest and remain unbiased in their recommendations and advice.

How can you know for certain that an advisor you’re interviewing is a fiduciary? The firm will either be listed as a Registered Investment Advisor or the advisors on the team will hold certifications that hold them to the fiduciary standard, such as the CERTIFIED FINANCIAL PLANNER™, Chartered Financial Analyst®, or Certified Public Accountant professional designations. Keep in mind, if the advisor doesn’t fit those descriptions, they may still act as a fiduciary in certain situations, like sharing a recommendation, but not necessarily when selling products.

Because it’s impossible to know for certain when someone is acting as a fiduciary versus a product salesman, it can be more difficult to trust an advisor who is not a fiduciary 100% of the time. Keeping this in mind as you vet potential candidates can help you avoid undisclosed conflicts of interest and find the right advisor for your unique needs.

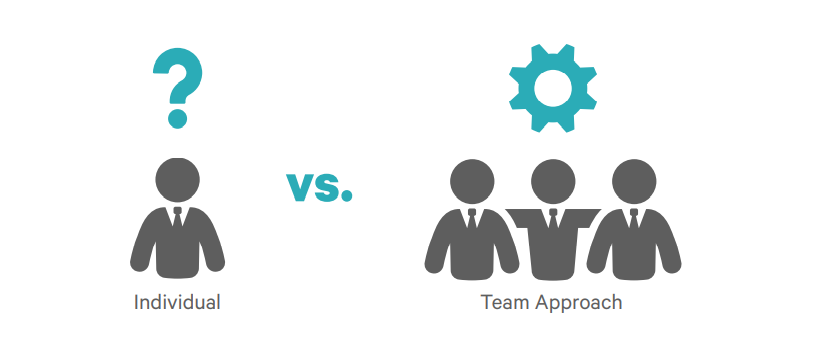

8. Not Hiring a Team

At some firms, you may work with only one person, while other firms may have a team approach. This is an important consideration when hiring an advisor. You may assume that a one-on-one relationship is the best way to develop true trust and receive the best level

of service, but this is a common misconception.

It’s better to work with a team so that your main point of contact always has backup. If you were to work with just one person, what would happen if they went on vacation, retired, or suddenly became ill? You would have a disruption of service at the bare minimum. On the more severe end, you would find yourself looking for a new advisor yet again.

Not only does a team approach provide continuity to your financial plan, but it also provides a greater degree of expertise and a broader range of knowledge.

It’s never a bad idea to have a second, or even third set of eyes working on your plan.

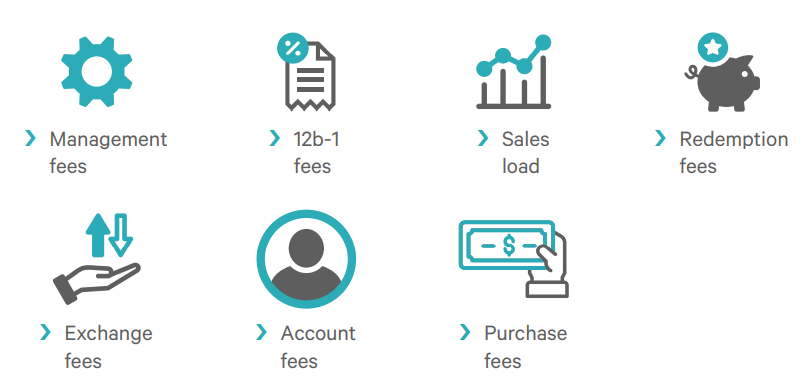

9. Not Investigating the Underlying Costs of Your Investments

Many people don’t realize how much goes into the cost of various investments. It’s not just a sticker price; there are often underlying fees that can drive the cost up significantly.

Let’s take a look at mutual funds, for example. They are one of the most popular ways to invest in a large variety of assets with relative ease. However, some mutual funds charge much higher fees than others, including:

Aside from wanting to get the best bang for your buck, understanding the cost of your investments can have a big impact on your long-term return. According to a recent Vanguard study, lower-cost investments actually perform better than higher-cost investments.

A good advisor should be willing to discuss the costs associated with their investment recommendations and help you find low-cost alternatives.

10. Letting Your Financial Advisor Lead With Investments

Lastly, don’t let your financial advisor lead with investments. There is no way an advisor can accurately assess your needs and recommend an appropriate investment strategy within the first hour of meeting you. If your advisor is asking for past investment

statements, designing a prospective portfolio, or making specific recommendations before they’ve even asked about your goals or risk tolerance, chances are they are not creating a strategy tailored to your needs.

Investments should be one component of a comprehensive financial plan—and a good advisor will tell you that. Look for an advisor who leads with planning and is willing to spend the first several meetings getting to know you, outlining your goals, and gathering information about your current financial situation, all before discussing specific investment recommendations.

Once your advisor has offered investment recommendations, don’t be afraid to ask why they are recommending particular services and solutions over others.

Aside from wanting to get the best bang for your buck, understanding the cost of your investments can have a big impact on your long-term return. According to a recent Vanguard study, lower-cost investments actually perform better than higher-cost investments.

If the solution is truly customized to your needs, the advisor should be able to thoroughly explain why one strategy was chosen over another.

Don’t Make These Mistakes

When Hiring a Financial Advisor

Are you looking for a financial advisor in Charlotte but you’re unsure where to start? Do you want to work with a fiduciary who is committed to always putting your needs first? At Calamita Wealth Management, we are here for you. Our fee-only, comprehensive financial planning process has helped affluent individuals and families throughout the country. With over 25 years of experience, we are passionate about serving our clients as fiduciary financial advisors. Schedule an introductory phone call using our online calendar or reach out to us at (704) 276-7325 or myretirement@calamitawealth.com.